I think the title of The Eight Wonder of the World has been quite overused, at this point, so I am going to skip over it and go right to The Ninth Wonder of the World. Make Sense?

This from The Board of Governors of the Federal Reserve System:

“The supplementary leverage ratio generally applies to financial institutions with more than $250 billion in total consolidated assets. It requires them to hold a minimum ratio of 3 percent, measured against their total leverage exposure, with more stringent requirements for the largest and most systemic financial institutions. The change would temporarily decrease tier 1 capital requirements of holding companies by approximately 2 percent in aggregate.”

The supplementary leverage ratio determines what percentage of deposits has to actually be held by a banking/lending institution. The rest can be loaned and/or invested. I thought the requirement was 10%, but am learning differently. It appears that smaller institutions are still required to keep 10% on-hand but larger institutions have less stringent requirements.

The reference above is to a “supplementary leverage ratio,” a term that is new to me. I always understood this scheme to be referred to as “fractional banking.

Now before I get too far down into the weeds, allow me, please, to make the point about the above info from the Fed. On April 20th, 2020, “To ease strains in the Treasury market resulting from the coronavirus and increase banking organizations’ ability to provide credit to households and businesses…” the Fed relaxed the leveraged requirement to 2% with a sunset clause of March 31st, 2021… in other words, in two weeks, it returns to 3%. Some think there is going to be an adverse reaction when this occurs.

The thinking, as I understand it, from Bill Sardi, writing on LewRockwell dot com, goes like this: “An expected return to higher bank leverage ratios on March 31st may result in negative interest rates on banked money and subsequent over-consumption with run-away inflation, bank runs with hoarding of paper money, as well as increased demand to own US-minted gold and silver coins.”

I am, frankly, unqualified to comment on this situation. I wish I knew more but I don’t. As for “US-minted gold and silver coins”… I have always been a big advocate of precious metals. Not only do I keep my own stock but I have been plying my children and grandchildren with the stuff for years as holiday gifts. I figure that when a grandkid reaches seventeen and has years before forgotten the Barbie’s and video games as gifts, they can look in their lockboxes and see all the silver and gold I gave them and have something to hold that has value.

Now, don’t get me wrong, I’d love to have kept some of the, now-valuable, musical instruments I sold, to give them, it’s just that I never was very good at looking into the crystal ball.

Okay, moving along, I do wish to write about something I have researched in the past: FRACTIONAL BANKING.

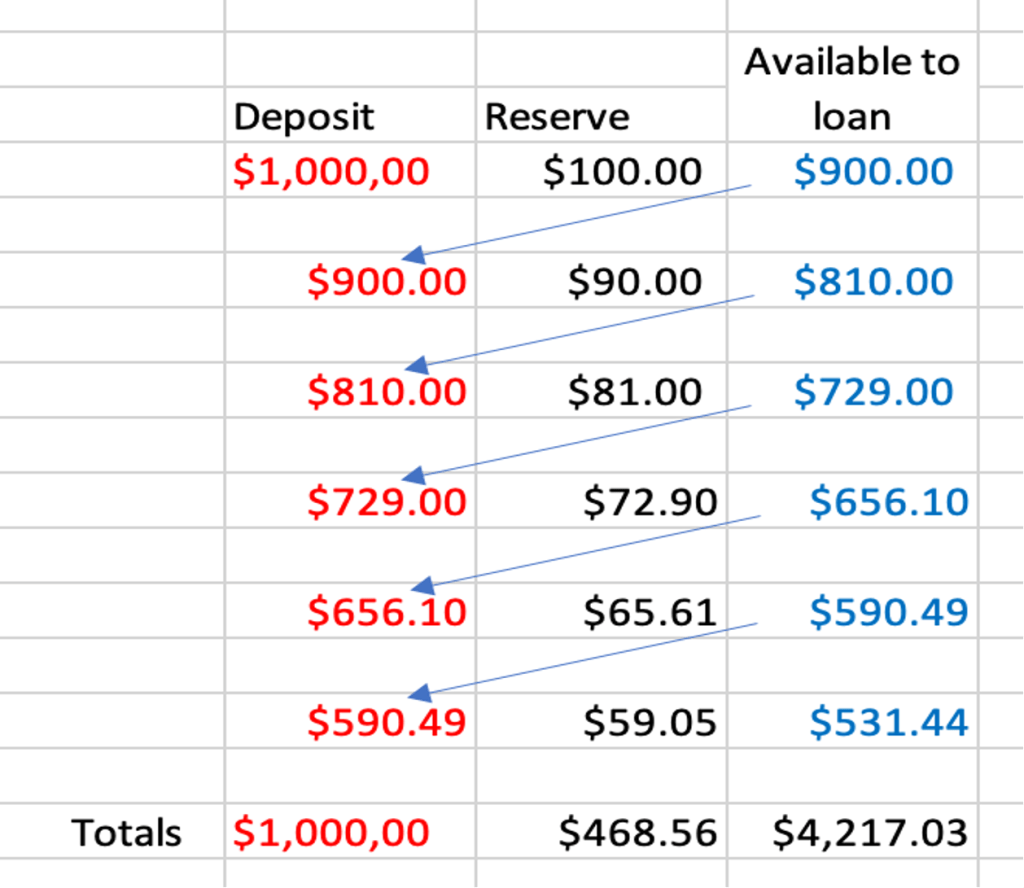

The chart I have attached explains how it works. You don’t have to do too much math before you start to see the problem. As stated, when a depositor puts $1,000 in the bank the bank is only required to hold 10% of that deposit in its vault, so to speak. The other 90% is available to loan. Now if a borrower takes his/her loan and opens up a business account, using the loan as working capital, that deposit is a separate deposit and falls under the same guidelines required for all deposits. Now, although my chart is simplified, you don’t have to go too far to see what I see as a potential problem. In fact, an additional part of this scheme is the FDIC – Federal Deposit Insurance Corporation – and banks pay a portion of their receipts to secure this coverage, and there are limits to how much of an account is insured. I believe the insured limit is currently $250,000 per depositor, $500,000 for joint depositors, per bank, per account ownership category. I do not know what “account ownership category” means. Does it mean one could keep 10 accounts and be insured in each one at $250k? Is Savings one category and Checking another category. I’m not sure. Anyway, if there is a run on the bank, and it cannot cover all of its deposits, the FDIC bails it out. This works on a limited basis… too many banks start to collapse and all bets are off.

As the chart shows, based on an original deposit of $1,000.00, the bank could loan out over $4,000.00 while holding only $468.56 in reserve. Nice work if you can get it.

Well, there you have the wonders of high finance. So, will there be a hiccup on March 31st, when the leverage ratio returns to 3%? Good question. If you come up with the answer to that, please let me know.